Learn how to record an Owner Contribution in your bookkeeping records for your handmade or creative business.

An Owner Contribution is:

- money that you take out of your own pocket or the family finances/budget to fund your handmade or creative business

- NOT Income for your business

- tracked on the Balance Sheet in the Equity Section

Often times, when you start your business you’ll take money out of your own pocket to get things started. Perhaps you’ll use this money to purchase:

- a domain name

- website hosting

- inventory

- an educational course

- to start an Etsy shop

- or, to open a business checking account

Other times, you may need to simply take money out of your own pocket to pay business expenses simply because your handmade or creative business isn’t generating enough revenue.

Many of the handmade business bookkeeping spreadsheets that I’ve found, including the one from Crochetpreneur, don’t provide you with a way to track money that you put into your business. And that doesn’t help you at all when it’s time to look at your big picture finances.

How to record an Owner Contribution

If you use bookkeeping software:

Most bookkeeping software programs automatically creates an Equity account for you when you create your Chart of Accounts.

The problem with this is that it doesn’t specifically create an account to track just the money you put into your business. But it’s easy enough to add a new Equity account that you’ll use just to keep track of the money your invest.

Once you have the new “contribution” tracking account, it’s super simple to record the transaction.

- open your checking account register

- enter the date

- in the deposit column, enter the amount

- and select the Owner Investment (or contribution) account

- record or save the transaction

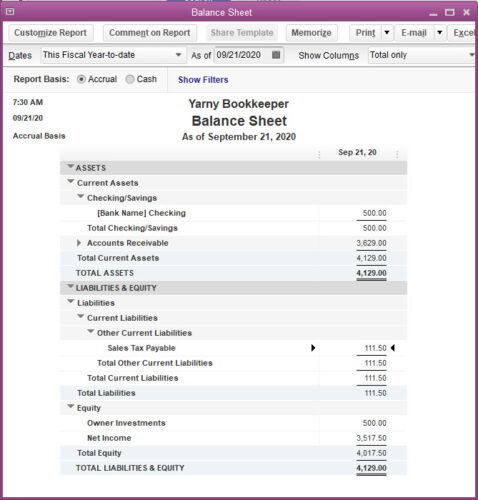

Once you record the deposit, both the checking account and the Owner Investment account, increase by the amount of the deposit and is shown on your Balance Sheet.

Now, at any point you can create a Balance Sheet Report in your software (I’m using QuickBooks Premier Desktop) and you can see how much money you’ve taken out of your pocket to fund your business.

The beauty of doing your bookkeeping in software, is that you can create a Balance Sheet for any date range that you want:

- This month

- This quarter

- Last quarter

- This year

- Last year

- Or, from the very moment that you started using software

If you’re using spreadsheets for your bookkeeping:

Spreadsheets are unique to the person that created them, they may or may not include a Balance Sheet or any other means of keeping track of the money you put into your business.

And that doesn’t help you make good business decisions, like is my business making enough money to support itself.

If your spreadsheet system doesn’t include a Balance Sheet or a way to keep track of the money that you put into your business, then I would highly recommend that you create a new “sheet” and keep track of it.

Did you find this post helpful?

[BTEN id=”5344″]

If you'd rather be working with yarn, fabric, paint or clay than deal with a pile of receipts or bookkeeping spreadsheets, you're in the right place.

I help you get a handle on your numbers, make sense of what's coming in and going out, and actually feel confident running your business -- without accountant-speak or guilt.

👉 Want help figuring out your bookkeeping (without overcomplicating it)? Join the Free Handmade Business Bookkeeping community.

I am a coach/educator, not your bookkeeper or CPA. This information is for educational purposes, NOT financial or tax advice.

Full Disclosure - How I use AI

I use AI to create blog post images, because it produces better maker specific images than I can find after spending hours searching through Canva and other places.

I write ALL of my own blog posts (sales pages, etc.), but I do run the draft through AI to make sure it's clear (and so I don't get too wordy or go off on a tangent!).

- Other Income and Other Expenses Explained for Handmade Business Owners - July 30, 2026

- Overhead Expenses Demystified for Handmade Business Owners - July 27, 2026

- A Handmade Product Pricing Calculator That Includes COGS - July 19, 2026

[…] In bookkeeping terms, that’s usually called an Owner Investment or Owner Contribution. […]