A lot of handmade business owners pay attention to the Profit & Loss Report and ignore the Balance Sheet. I get it. The Profit & Loss feels easier to understand because it shows sales, expenses, and profit. The Balance Sheet can feel like the weird report sitting off to the side that nobody really wants to deal with.

But your Balance Sheet matters more than a lot of makers realize.

If you use real bookkeeping software, your Balance Sheet Report is usually sitting right there waiting for you. If you use spreadsheets, that is a whole different animal. A true Balance Sheet usually is not built in because it takes a lot more structure behind the scenes to make one work properly. That is one reason so many makers have never paid much attention to it.

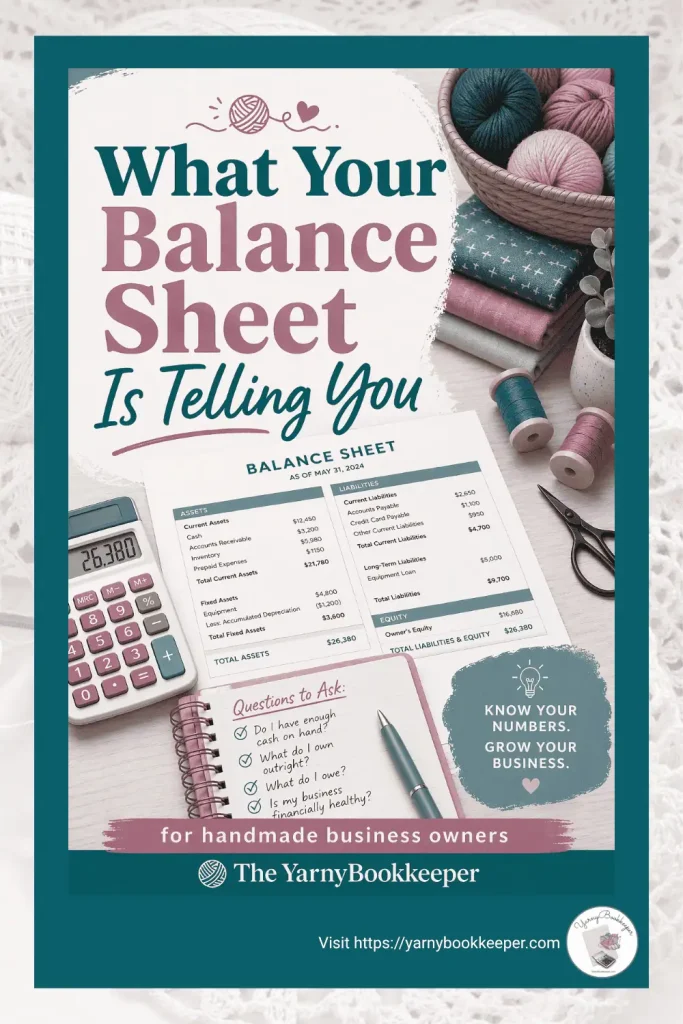

A Balance Sheet gives you a snapshot of what your business owns, what it owes, and what is left over for you as the owner. It can also help you spot problems that do not always show up clearly on your Profit & Loss Report.

If your numbers feel confusing, your cash feels tight, or you are not sure whether your bookkeeping actually reflects what is happening in real life, your Balance Sheet has something to say about that.

Short on time? Here are five things your Balance Sheet may be telling you.

- What you own

- What you owe

- What’s yours

- What’s tied up in inventory

- Your numbers may not match real life

- A simple way to think about your Balance Sheet

- Why a Balance Sheet matters

- What to check each month

- Final Thoughts

Here’s the 5 Things Your Balance Sheet Is Telling Your About Your Handmade Business

1. Here’s what your business owns

The first thing your Balance Sheet shows you is your business assets.

Assets are the things your business owns or controls that have value. In a handmade business, that might include your checking account balance, savings set aside for taxes, materials inventory, finished products, equipment, or money that customers still owe you.

This matters because a Balance Sheet is not just about cash. A maker can look at the bank account and think there is not much there, while the Balance Sheet shows that money is tied up in inventory, supplies, or other business assets.

In other words, this report helps you see the full picture, not just the cash sitting in one account.

2. Here’s what your business owes

The next thing your Balance Sheet shows you is your liabilities.

Liabilities are debts and obligations your business owes to someone else. That might include a business credit card, a loan, unpaid bills, sales tax you have collected but not remitted yet, or payroll liabilities if that applies to your business.

This section is important because it reminds you that not all of the money sitting in your business belongs to you. Some of it may already have a job. It may need to go toward paying suppliers, paying down debt, or sending sales tax where it belongs.

That is one reason a business can have money coming in and still feel tight. The money may already be spoken for.

3. Here’s what is actually yours as the owner

Your Balance Sheet also shows owner’s equity.

In plain English, owner’s equity is what is left after liabilities are subtracted from assets. It reflects your stake in the business.

A simple way to think about it is this: if your business sold off everything it owned and paid everything it owed, owner’s equity is what would be left for you.

For a sole proprietor or single-member LLC, this section is usually affected by a few things:

- money you put into the business

- money you take out of the business

- profits

- losses

That means owner’s equity does not change for just one reason. It can go up because the business made money or because you put money in. It can go down because the business ran at a loss or because you took money out.

This is one of the reasons it helps to look at your Balance Sheet regularly. If your equity keeps shrinking, it is worth paying attention to. It does not automatically mean disaster, but it does mean something is changing and you should understand why.

4. You may have more money tied up in inventory than you think

This is a big one for handmade business owners.

A lot of makers do not realize how much money can get tied up in materials, unfinished products, or finished inventory sitting on shelves. On paper, that inventory is an asset. In real life, it can still leave your cash feeling squeezed.

That is one reason a business can look fine at a glance while the owner feels like there is never enough money in the bank.

If too much cash is getting poured into supplies or products that are not selling fast enough, your Balance Sheet can help you see it. It will not solve the problem for you, but it can point you in the right direction.

This is especially helpful if you have ever said something like, “I’m making sales, so why does my bank account still feel so sad?”

Sometimes the answer is not that the money disappeared. It is that the money got turned into inventory.

5. Your numbers may not match real life

One of the most useful things about the Balance Sheet is that it helps you catch bookkeeping problems.

If something looks off, that report can wave a flag.

Maybe your checking account balance on the Balance Sheet does not match what is actually in the bank. Maybe your credit card balance looks wrong. Maybe sales tax payable seems too high or too low. Maybe inventory is sitting there at a number that does not make any sense. Maybe you forgot to record money you put into the business, or maybe owner draws have not been handled correctly.

The Balance Sheet is one of the best reports for catching those kinds of issues because it shows what your business says is true at that moment in time.

When the report does not match real life, that usually means something needs your attention.

A simple way to think about the Balance Sheet

At its core, the Balance Sheet is built on this idea:

Assets = Liabilities + Owner’s Equity

That is the bookkeeping version.

The plain-English version is this: everything your business owns had to come from somewhere. It either came from money the business owes, or from money that belongs to you as the owner.

You do not need to memorize the formula to make use of the report, but it helps to understand what the report is trying to show you.

Why this report matters for makers

If you run a handmade or creative business, your Balance Sheet is not just some accounting formality.

It can help you see:

- whether your business has cash available

- whether too much money is tied up in inventory

- whether you are carrying debt

- whether you owe sales tax

- whether you are putting your own money into the business to keep it going

- whether your bookkeeping is actually making sense

That is valuable information.

Even if you are a sole proprietor and you are not preparing a Balance Sheet for tax filing purposes, it is still one of the most useful reports you can review in your bookkeeping. It helps you understand what is going on behind the scenes, and it gives context to what you see on your Profit & Loss Report.

What to check on your Balance Sheet each month

You do not need to stare at this report for an hour. Just look for a few practical things.

Check whether your bank and credit card balances look right. Check whether your sales tax payable balance makes sense. Check whether your inventory looks reasonable. Check whether owner’s equity seems to be moving in a way you understand. If something jumps out at you and makes no sense, do not ignore it.

That confusion is usually trying to tell you something.

And if you use spreadsheets instead of bookkeeping software, this is also a reminder that some reports are much harder to build manually, which is one reason they often get skipped.

Final thoughts about what your Balance Sheet is trying to tell you

Your Balance Sheet may not be the flashiest report in your bookkeeping software, but it is one of the most useful.

It tells you what your business owns, what it owes, how much is really yours, and whether your numbers match reality. For handmade business owners especially, it can also show when cash is getting tied up in inventory or when the business is carrying more weight than you realized.

If you have been ignoring your Balance Sheet in your bookkeeping software because it feels intimidating, unnecessary, this is your nudge to start paying attention to it.

You do not need to become an accountant. You just need to understand what the report is trying to tell you.

If you'd rather be working with yarn, fabric, paint or clay than deal with a pile of receipts or bookkeeping spreadsheets, you're in the right place.

I help you get a handle on your numbers, make sense of what's coming in and going out, and actually feel confident running your business -- without accountant-speak or guilt.

👉 Want help figuring out your bookkeeping (without overcomplicating it)? Join the Free Handmade Business Bookkeeping community.

I am a coach/educator, not your bookkeeper or CPA. This information is for educational purposes, NOT financial or tax advice.

Full Disclosure - How I use AI

I use AI to create blog post images, because it produces better maker specific images than I can find after spending hours searching through Canva and other places.

I write ALL of my own blog posts (sales pages, etc.), but I do run the draft through AI to make sure it's clear (and so I don't get too wordy or go off on a tangent!).

- Other Income and Other Expenses Explained for Handmade Business Owners - July 30, 2026

- Overhead Expenses Demystified for Handmade Business Owners - July 27, 2026

- A Handmade Product Pricing Calculator That Includes COGS - July 19, 2026

[…] already talked about the Balance Sheet side of your business: assets, liabilities, and equity. Now we’re moving into the Profit & […]

[…] part of your Owners Equity, so it shows up on your Balance Sheet […]

[…] liabilities are one of the main sections of your Chart of Accounts and one of the big pieces on the Balance Sheet side of your […]

[…] the Chart of Accounts and how it gives your bookkeeping some structure. Now we’re moving into the Balance Sheet side of that map, starting with […]

[…] categories that feed information into two very important business financial reports – the Balance Sheet and the Profit & Loss or Income […]

[…] first is the Balance Sheet. This report shows what your business owns, what it owes, and what belongs to you. That is where […]

Very helpful article

Thank you 😀 I’m so glad you found it helpful.