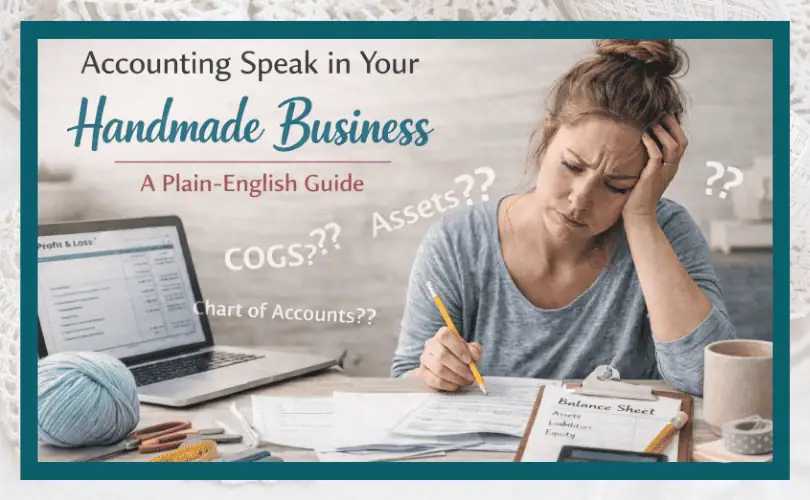

If you’ve ever opened up a Profit & Loss report, looked at your bookkeeping software, or talked to a CPA or tax preparer and thought, “I have no idea what half of these words mean,” you are not alone. That’s accounting speak.

A lot of handmade business owners end up feeling behind because they keep running into accounting terms nobody ever explained in plain English. You hear words like assets, liabilities, equity, cost of goods sold, overhead, or chart of accounts, and suddenly it feels like everybody else got the secret handbook except you.

That can make bookkeeping feel a whole lot harder than it actually is.

A lot of the time, the real problem is not that you are bad at business or incapable of understanding your numbers. It’s that the language is getting in the way first.

And when the vocabulary feels confusing, everything else starts to feel heavier too. Reports look intimidating. Bookkeeping decisions feel shakier than they need to. Conversations with accountants or tax pros get frustrating fast.

That’s exactly why I created this series.

This series is here to help you make sense of the accounting terms that show up in your handmade business, explain what they actually mean, and show you how they fit together. Not in stiff accountant language. Not in a way that makes your eyes glaze over. Just plain English, with examples that actually make sense for makers.

Once the words start making sense, the rest gets a lot easier.

New to this series? Start with this post, then work through the rest in order.

Short on time? Here’s the key topics in this post:

- Why accounting terms matter in a handmade business

- The big picture: the main accounting categories

- The two main reports these categories feed into

- How this series is organized

- The Accounting Speak series for handmade business owners

- Where to start next

| If you’d like a simple, all-in-one resource to go with this series, grab my free guide: Accounting Speak for Handmade Business Owners. It includes plain-English explanations of the bookkeeping terms makers run into most often, along with workbook pages to help you sort out what those terms mean in your own business. |

Why accounting terms matter in a handmade business

Accounting terms show up all over the place, whether you like it or not.

You’ll see them in bookkeeping software, spreadsheets, financial reports, tax conversations, blog posts, educational content, and year-end paperwork. Even if you are doing your bookkeeping in a simple way, the language still tends to show up sooner or later.

And if you don’t understand the words, it gets a lot harder to understand what your numbers are really telling you.

For example, if you don’t know the difference between inventory and expenses, it becomes much easier to track your materials the wrong way. If you don’t understand cost of goods sold, it becomes harder to see what it actually costs to make and sell your products. If terms like liability or equity sound vague and abstract, then reports like the Balance Sheet start feeling like a bunch of nonsense.

That matters because the point of bookkeeping is not just to “keep records.” The point is to help you understand what is happening in your business.

You do not need to sound like an accountant. You just need enough clarity to understand your reports, organize your bookkeeping, and stop feeling lost every time financial jargon shows up.

The big picture: the main accounting categories

Before we dig into the individual posts in this series, it helps to start with the big picture.

Most of the accounting terms you run into in a handmade business fall into a few main categories. Once you understand those categories, the rest starts feeling a lot less random.

Assets

Assets are things your business owns or has available to use.

That might include the money in your business bank account, your inventory, your materials and supplies, your equipment, or anything else your business owns that has value.

So if you have yarn on the shelf, clay ready to use, a label printer, or cash sitting in your checking account, those are all examples of assets.

Liabilities

Liabilities are things your business owes.

That could be sales tax you collected and still need to send in, a balance on your business credit card, a loan, or bills you haven’t paid yet.

In other words, liabilities are obligations. It’s money that is not really yours to keep, or money your business still has to pay.

Equity

Equity is the owner’s share of the business.

A simple way to think about it is this: after you look at what the business owns and subtract what it owes, what is left belongs to you. That is the basic idea behind equity.

This is one of those words that sounds more dramatic than it needs to be. It is really just part of the overall structure of how the books are organized.

Income

Income is money coming into your business from the things you sell or the work you do.

For a handmade business, that might include finished product sales, custom orders, pattern sales, classes, workshops, wholesale orders, or other regular revenue streams.

This is the category most people naturally pay attention to first, because it feels the most obvious. Money comes in, so that must be income.

And yes, that part is pretty straightforward.

Cost of Goods Sold

Cost of Goods Sold, often shortened to COGS, is one of the terms that confuses handmade business owners the most.

This is the direct cost tied to the products you actually sold.

Depending on your business, that might include the yarn, fabric, clay, beads, wood, wax, or other materials that went into sold items. It can also include certain packaging or production-related costs tied directly to what was made and sold, including booth and merchant fees,

This matters because it helps answer a very important question: what did it cost you to make and sell the thing you sold?

That is different from general business spending, and it deserves its own category.

Overhead Expenses

Overhead expenses are the regular costs of running your business that are not directly tied to making one specific product.

That might include things like website fees, bookkeeping software, internet, office supplies, education, or advertising.

These are the costs of keeping the business running in general.

They matter, but they are not the same as the direct cost of the products you make and sell.

Other Income

Other Income is money that comes into the business that is not part of your normal sales activity.

Depending on your business, this could include affiliate income, ad revenue, cashback rewards, or some other occasional source of money that does not belong under your regular product or service income.

It usually does not come up as often as regular sales, but it still needs a proper place when it does.

Other Expenses

Other Expenses are costs that do not fit neatly under your regular operating expenses.

This category tends to be more occasional and more situational. It is not where everyday spending belongs, but it can matter when something unusual comes up and needs to be tracked separately.

The two main reports these categories feed into

As you learn these terms, it helps to know that they usually end up on one of two main financial reports.

The first is the Balance Sheet. This report shows what your business owns, what it owes, and what belongs to you. That is where you’ll find assets, liabilities, and equity.

The second is the Profit & Loss, sometimes called the income statement. This report shows how your business performed over a period of time. That is where you’ll find income, cost of goods sold, overhead expenses, other income, and other expenses.

You do not need to memorize all of that right now. The point is just to start seeing the map.

Once you can see the map, the individual terms stop feeling so random.

How this series is organized

To make this easier, I broke the series into three phases.

In Phase 1, we start with the big picture. This is where you learn the basic structure and begin to see how the categories fit together.

In Phase 2, we move to the Balance Sheet side of things. That is the part that deals with what your business owns, what it owes, and what belongs to you.

In Phase 3, we move to the Profit & Loss side. That is where we look at the categories that affect profitability and help you understand what is really going on with your money.

This way, instead of trying to swallow a bunch of accounting jargon all at once, you can work through it one piece at a time.

In a hurry? Start with the Chart of Accounts post if you want to see how these terms show up in real bookkeeping.

The Accounting Speak series for handmade business owners

Here’s the full series so you can work through it in order.

Phase 1: Learn the map

1. Accounting Speak in Your Handmade Business: A Plain-English Guide

You’re here. This post gives you the big-picture overview and helps you see how the main accounting terms fit together.

2. Chart of Accounts Explained for Handmade Business Owners

This post explains the Chart of Accounts, which is basically the master list of categories that organizes your bookkeeping and financial reports.

Phase 2: The Balance Sheet side

3. Assets

What your business owns or has available to use, like cash, inventory, supplies, and equipment.

4. Liabilities

What your business owes, like sales tax, credit cards, loans, and unpaid bills.

5. Equity

The owner’s share of the business and where that fits into the overall picture.

Phase 3: The Profit & Loss side

6. Income

The money your business earns from the things you sell and the work you do.

7. Cost of Goods Sold

The direct costs tied to the products you make and sell.

8. Overhead Expenses

The general costs of running your business that are not directly tied to one specific item.

9. Other Income + Other Expenses (coming 8/2/2026)

The categories for money in or out that does not fit neatly into your regular sales or regular operating expenses.

| Want the workbook-style version of this series in one place? Grab the free Accounting Speak for Handmade Business Owners guide. |

Where to start next

If you’re brand new to all of this, the best next step is the Chart of Accounts post.

That is usually where things start clicking for handmade business owners, because it shows how all these terms actually get used in real bookkeeping.

Once you understand that structure, the rest of the series gets a whole lot easier to follow.

You do not need to become an accountant.

You do not need to memorize a bunch of jargon just to be a “real” business owner.

You just need the words to stop sounding like nonsense.

That’s what we’re doing here, one piece at a time.

If you'd rather be working with yarn, fabric, paint or clay than deal with a pile of receipts or bookkeeping spreadsheets, you're in the right place.

I help you get a handle on your numbers, make sense of what's coming in and going out, and actually feel confident running your business -- without accountant-speak or guilt.

👉 Want help figuring out your bookkeeping (without overcomplicating it)? Join the Free Handmade Business Bookkeeping community.

I am a coach/educator, not your bookkeeper or CPA. This information is for educational purposes, NOT financial or tax advice.

Full Disclosure - How I use AI

I use AI to create blog post images, because it produces better maker specific images than I can find after spending hours searching through Canva and other places.

I write ALL of my own blog posts (sales pages, etc.), but I do run the draft through AI to make sure it's clear (and so I don't get too wordy or go off on a tangent!).

- Overhead Expenses Demystified for Handmade Business Owners - July 27, 2026

- A Handmade Product Pricing Calculator That Includes COGS - July 19, 2026

- Cost of Goods Sold for Makers: What It Means and Where Product Costs Belong - July 19, 2026

[…] if the bookkeeping words themselves make your brain glaze over, this Accounting Speak guide can help you understand the basic terms without the fancy-pants […]

[…] the Accounting Speak series, we’ve already looked at Income and Cost of Goods Sold. Now we’re looking at the regular […]

[…] talk about income in plain English, without the accountant-speak headache. This is part 6 of our Accounting Speak in Your Handmade Business […]

[…] It’s not scary. It’s just one more piece of the bookkeeping map. […]

[…] Just popping in? This is part 3 of our Accounting Speak in Your Handmade Business Series, to find and read about the entire series, click here. […]