If you’ve been following along in the Inventory + COGS series, you already know what inventory is and how to track it.

So let’s zoom out for this final piece and answer the question that really matters:

👉 When does all of this actually hit your bookkeeping (and your taxes?)

Because understanding when inventory and Cost of Goods Sold hit your books is one thing… Seeing how that timing shows up on your tax return is where most handmade sellers finally have their ohhhhhh moment.

This Is a Review — Not a How-To

At this point in the series, we’ve already covered:

- What counts as inventory

- How materials and finished items are tracked

- Why Cost of Goods Sold matters

- How inventory moves inside your bookkeeping system

So instead of repeating that, this post is here to connect the dots between:

Your bookkeeping records → your Profit & Loss → your Schedule C

This is where timing matters.

The Tax Rule That Drives Everything

Here’s the rule the IRS cares about most:

👉 You cannot deduct materials and supplies when you buy them.

👉 You deduct them when the finished item sells.

That’s why inventory exists in the first place.

Your bookkeeping isn’t being difficult. It’s just following tax law.

Why Inventory Feels “Delayed” on Your Taxes

From a tax perspective, inventory is considered an asset, not an expense.

That means:

- Buying yarn, fabric, clay, or supplies does not lower your taxable income right away

- Those costs sit in inventory until a sale happens

- Only then do they become Cost of Goods Sold

This is why you can spend money in one year… and not see a deduction until a completely different year.

How This Timing Plays Out Across Tax Years

Year 1 (2018)– You Buy Supplies

- Inventory purchases show up on your books

- Inventory value appears on your Balance Sheet

- Cost of Goods Sold = $0

- Nothing is deducted yet

👉 On your Schedule C, inventory is reported — but not expensed.

Year 2 (2019) – You Make Items (But Don’t Sell Them)

- Costs move around inside inventory (materials → finished items)

- Total inventory value adjusts based on purchases

- Still no sales

- Still no Cost of Goods Sold

👉 Your Schedule C reflects inventory activity, not deductions.

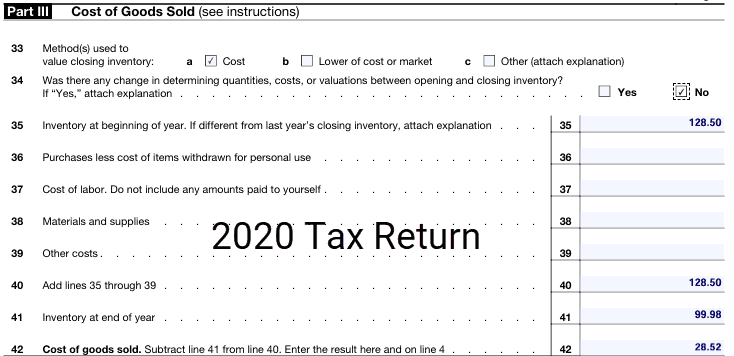

Year 3 (2020) – You Finally Make a Sale

This is the turning point.

When a finished item sells:

- No new purchases

- The sale price shows up as Income

- The cost to make that item finally moves out of inventory

- That cost becomes Cost of Goods Sold

- Your profit is now reduced by that amount

👉 This is the year the deduction actually happens.

Why Your Schedule C Looks the Way It Does

When you look at Part III – Cost of Goods Sold on your Schedule C, it’s basically a summary of everything your inventory tracking has been doing all along.

It pulls from:

- Beginning inventory

- Purchases

- Ending inventory

And from that, the IRS calculates: Cost of Goods Sold

That’s why:

- No sales = no COGS

- Inventory still appears even if nothing sold

- Your “expenses” don’t always match your spending

Your tax return is simply reflecting timing, not mistakes.

This Is Why Good Inventory Records Matter

All those inventory details you’ve been tracking? They’re not just for your own sanity.

They’re what make the Cost of Goods Sold section of your tax return:

- accurate

- defensible

- far less stressful

When inventory is done correctly, your Schedule C practically fills itself in.

Want to See This Inside Real Bookkeeping Records?

If you want to see how this inventory-to-COGS timing looks inside bookkeeping spreadsheets — including how costs move year to year — that’s exactly what I walk through in the previous part of this series.

👉 Watch the walkthrough and then come back here to see how it lands on your tax return.

The Big Takeaway

If your profit ever feels “off,” or your taxes don’t reflect how much you feel like you spent, inventory timing is usually the reason.

Nothing is missing. Nothing is wrong. It’s just waiting for the sale.

And once you understand when inventory and COGS hit your books — and your taxes — the whole system finally clicks.

And because tax season has a way of making maker brains spiral… here are the most common “wait—WHAT?!” questions I hear about inventory + COGS.

“If inventory + COGS timing still feels fuzzy, the 10-Minute Bookkeeper walks you through it step by step.”

👉 This is Part 8 of the “Inventory + COGS for Handmade Businesses: Start Here series”. Access the series here.

Quick Tax-Time Panic FAQ (for Handmade Sellers)

I spent a bunch on supplies … why doesn’t it look like I ‘deducted’ it?

Yes, the money to pay for the supplies came out of your checking account (or hit your credit card), so that’s all good.

BUT, inventory doesn’t work like regular expenses. If those supplies are meant to make products you sell, the cost usually sits in Inventory until the item sells. Then it becomes COGS.

So …… what year does it count?

In most cases:

- Buy supplies –> counts as inventory (not a deduction yet)

- Make the item –> still inventory

- Sell the item –> the cost becomes COGS (that’s when it hits your taxes)

What if I made a ton of items but didn’t sell anything this year?

Then you likely won’t have COGS (or it’ll be very small), even if you spent money. Your costs are still there — they’re just sitting in Ending Inventory waiting for a sale year.

My profit looks “too high” this year ….. am I going to owe a ton in taxes?

Maybe (I honestly can’t say as I’m not your tax pro or bookkeeper and don’t know the BIG picture). But inventory timing is often why. If you had low sales but high purchases, your purchases may not be deductible yet, which can make profit look higher on paper. This is one reason inventory tracking matters so much – remember it’s money sitting on your shelves.

Do I have to track inventory if I’m small?

Often, yes — especially if you’re making and selling physical products. (And even when you qualify for small-business exceptions, you still need consistent records to support your numbers at tax time.)

What numbers should I double-check before I file?

At a minimum:

- Beginning Inventory (last year’s ending inventory)

- Purchases for the year

- Ending Inventory (your count/value at year-end)

- And that your bookkeeping method matches what you’re putting on Schedule C Part III

HELP! I think I messed this up last year.

You’re not alone. Inventory is one of the most commonly confused areas for handmade sellers. If last year’s numbers were off, don’t panic — you can usually clean it up by getting a solid year-end count, making your records consistent, and fixing the flow going forward (and getting pro help if the numbers are big or messy).

If you'd rather be working with yarn, fabric, paint or clay than deal with a pile of receipts or bookkeeping spreadsheets, you're in the right place.

I help you get a handle on your numbers, make sense of what's coming in and going out, and actually feel confident running your business -- without accountant-speak or guilt.

👉 Want help figuring out your bookkeeping (without overcomplicating it)? Join the Free Handmade Business Bookkeeping community.

I am a coach/educator, not your bookkeeper or CPA. This information is for educational purposes, NOT financial or tax advice.

Full Disclosure - How I use AI

I use AI to create blog post images, because it produces better maker specific images than I can find after spending hours searching through Canva and other places.

I write ALL of my own blog posts (sales pages, etc.), but I do run the draft through AI to make sure it's clear (and so I don't get too wordy or go off on a tangent!).

- Overhead Expenses Demystified for Handmade Business Owners - July 27, 2026

- A Handmade Product Pricing Calculator That Includes COGS - July 19, 2026

- Cost of Goods Sold for Makers: What It Means and Where Product Costs Belong - July 19, 2026

[…] When Inventory & COGS Actually Hit Your Bookkeeping (And Your Taxes)The “where does this go?” post — when inventory becomes COGS and what that looks […]

[…] is removed from Finished Items Inventory (or Consignment Inventory) and is moved so it hits the Cost of Goods Sold – Materials account on your Profit & Loss Report. And, what you sold it for hits […]