Tax time is almost here in the U.S. and that means it’s time to review your bookkeeping records and reports. For some of us, it may actually mean several days of grueling data entry. Either way, once the data is entered, you need to carefully review your reports for accuracy.

For most of us here in the U.S. we’ll be filing a Schedule C in addition to our regular Form 1040, be aware that the Form 1040 is much different this year than previous years. The changes are significant and I strongly suggest that you have a tax professional complete your taxes for you this year instead of doing them yourself.

When you own your own business – even if you enter all of your own data – it’s crucial that you review your bookkeeping records on a regular basis. Personally, I do it every month.

You’re probably thinking – why the heck do I need to review my records – I entered all the information to begin with!

Let’s see if I can answer that question for you.

Why do I need to review my bookkeeping records?

When we do our books, normally we are just focused on getting the information recorded and all those receipts out of the way and be done with it. Yes, we all find bookkeeping tasks to be our least favorite thing.

Once the information is entered, most people just close the spreadsheet or their software and say “WHEW, that crap is done, oh look I had $X of sales – not bad.”

If you don’t take the time to stop and review your Profit & Loss Report, you don’t see the bigger picture of:

- What were my total Sales this month?

- How much did the materials Cost?

- What else did I spend money on?

- Did I really make any money?

This big picture is really important.

Here’s a little example. Let’s say that you have a goal of having $500.00 of income every month or $6,000.00 a year:

- January Sales $1,000.00

- (MINUS) Cost of Goods Sold – $250.00

- (Equals) Gross Profit – $750.00 (not bad)

- (MINUS) Expenses/Overhead – $500.00

- (Equals) Net Income – $250.00 (YIKES)

At this point you would really want to stop and look at your Expenses/Overhead. What chewed up that $500.00? That’s when you really want to dig into where your money is going.

- Are you paying $50.00 a month for magazine or app subscriptions for things that you haven’t touched in months? If so, cancel those accounts!

- Did you spend $100.00 on office supplies? Ok, that’s probably legit – just watch out for Office Supply purchases over the next few months, they should be minimal or non-existent.

These are just a couple of things that could be eating up your Net Income every month!

What records & reports should you review?

You’re probably wondering what records and reports you should review and that’s a great question. In my day job as a software developer, professional bookkeeper and QuickBooks trainer, I have several of our customers that I work with on a regular basis. With some of them I do a quarterly review and with others it’s simply a year-end review. These are the reports that I always look at:

- A Profit & Loss report for the entire year, displayed by month

- A Balance Sheet Report (displayed by month if possible)

- An Inventory report

What should I look for when reviewing my records for tax time?

Whether you intend on doing your own taxes or hiring someone – you need to review all of your bookkeeping records before you even think about filing your tax return. If your tax preparer see’s something “odd”, they will make you dig to explain it. Better to do a thorough review beforehand.

The screenshot below showing a Profit & Loss report for the year and displayed by month (and you may want to open it in a new tab so it can be seen better) is from a Sample QuickBooks Company file. I’ve highlighted several things that send out a warning flag that your reports MIGHT be incorrect. This will simply give you an idea of WHAT to look for.

Here is a list of things to look for. In reality these entries could be 100% accurate, but these are the things that a tax preparer would and should question:

- A month where Cost of Goods Sold doesn’t seem to go with the Income. In the screenshot, look at the Aug column.

- Next, take a look at the Bank Service Charges category. Specifically, the Jan and Dec columns. It looks like normally the Bank Service Charge is $10 per month, but it’s higher in Jan and 0 in Dec.

- In the Marketing & Advertising category, the numbers are all over the place. It would appear that most months this company was spending $650, but there are some months where that amount is much higher.

- The Merchant Fees category is another warning sign…..how can you have Income with no merchant fees.

- The Outside Services category has nothing all year until you look at the Nov column

- In the Rent category, nothing is showing for the Dec column

- The Telephone category is another instance – nothing in Feb or Dec columns.

- Any month that has negative Income should be scrutinized carefully.

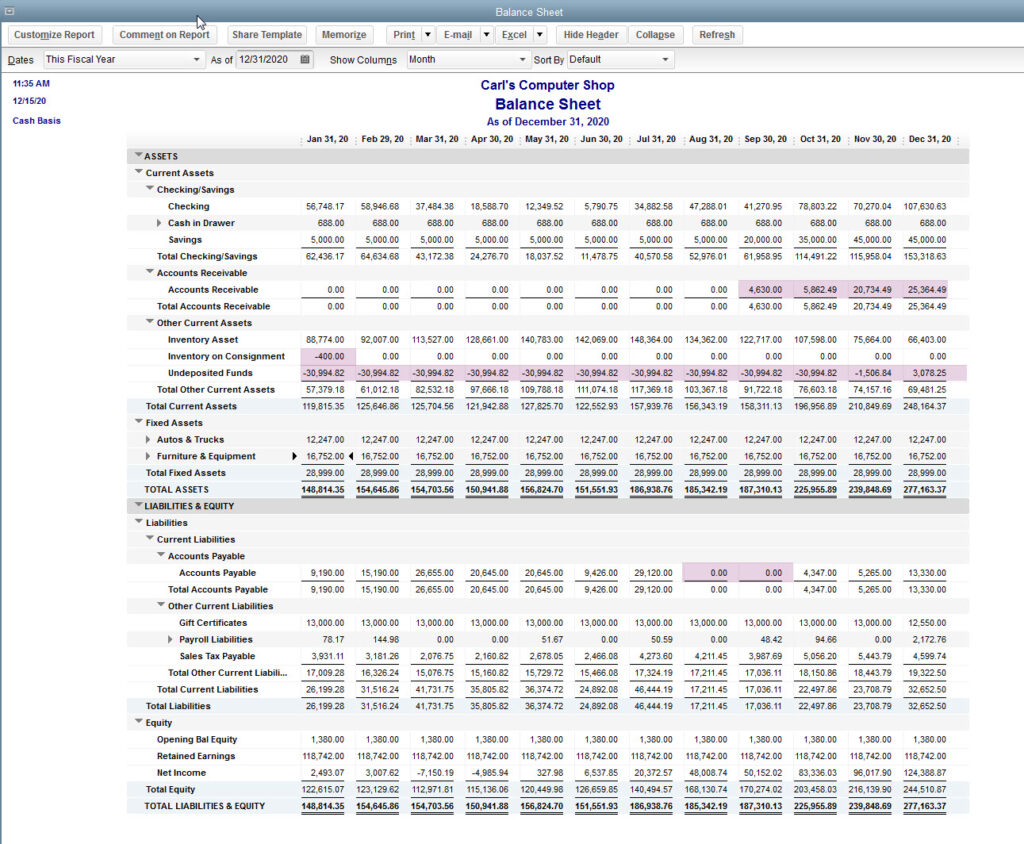

Next up, let’s look at a Balance Sheet report for the year, displayed by month.

Now a Balance Sheet report is a little harder to review, but here are some things that would stand out for me.

- Normally nothing in Accounts Receivable, but then amounts from September through December

- Negative amount in the Inventory on Consignment account. Inventory is an Asset and shouldn’t ever be a negative number.

- The Undeposited Funds account. Now this is a special QuickBooks account which holds money until it is deposited in your bank account. Think of a desk drawer where you put your checks until you actually put together a deposit slip and take those checks to the bank. It’s very seldom that this account should have a balance in it. And it should never have a negative balance.

- Accounts Payable normally has a balance, but all of a sudden in Aug and Sept there is nothing.

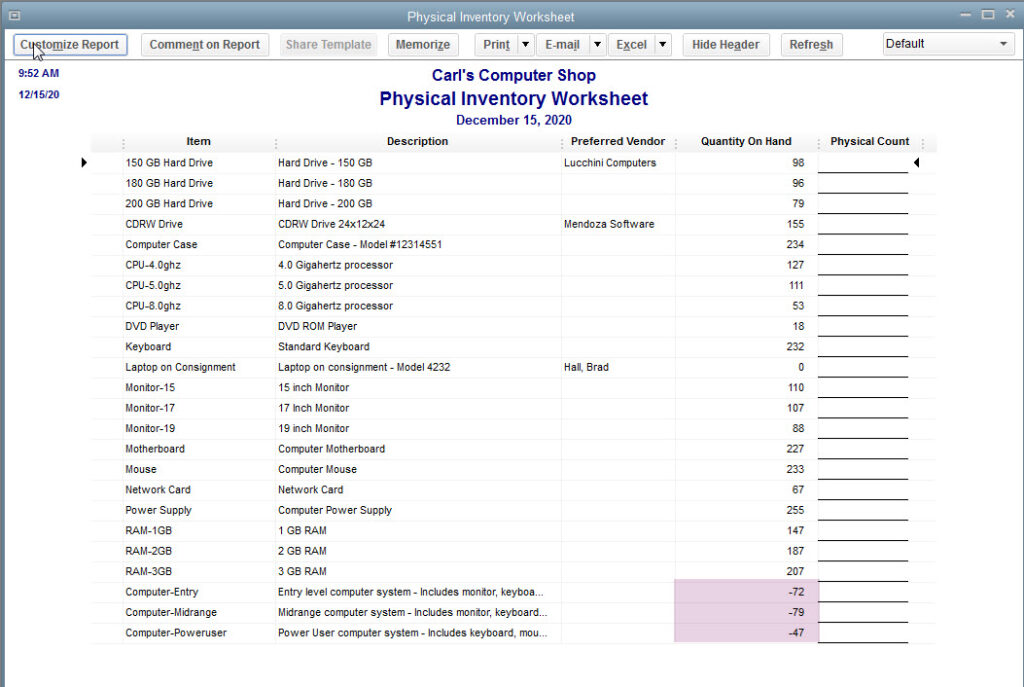

So, the last things we want to look at is a Physical Inventory Report from QuickBooks.

This report makes it easy to spot inconsistencies – how can you have negative inventory? This means that you literally sold more of something than you had available in inventory. In this instance you would want to carefully scrutinize your Cost of Goods Sold account because it would mean that you posted a purchase directly to COGS instead of inventory.

I hope you’ve found these tips to be helpful.

If you'd rather be working with yarn, fabric, paint or clay than deal with a pile of receipts or bookkeeping spreadsheets, you're in the right place.

I help you get a handle on your numbers, make sense of what's coming in and going out, and actually feel confident running your business -- without accountant-speak or guilt.

👉 Want help figuring out your bookkeeping (without overcomplicating it)? Join the Free Handmade Business Bookkeeping community.

I am a coach/educator, not your bookkeeper or CPA. This information is for educational purposes, NOT financial or tax advice.

- Chart of Accounts Explained for Handmade Business Owners - June 15, 2026

- Accounting Speak in Your Handmade Business: A Plain-English Guide - June 7, 2026

- A Realistic Budget Template for Handmade Business Owners - June 1, 2026